2025 Trends Report: The Technological Future of Polish Industry. An Analysis for Business Leaders in Key Regions

2025-09-29

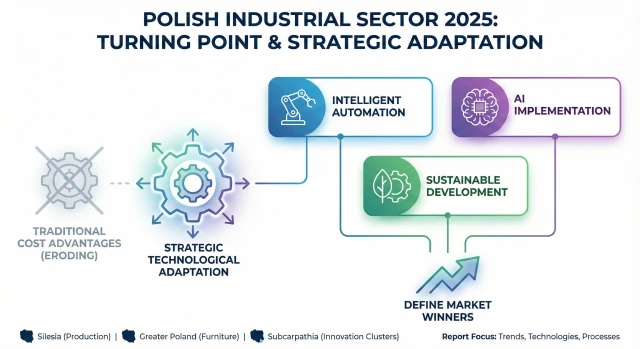

The picture of automation in Poland is full of contrasts. On one hand, 76% of companies see it as key to maintaining competitiveness. On the other hand, the data is unequivocal. The robot density in Polish industry is just 61 robots per 10,000 employees, while in the Czech Republic, this figure reaches 180, and in Hungary, 117. This "automation gap" poses a strategic risk that could weaken the position of Polish exporters.

-

Key Technologies: The new wave of automation is based on more flexible and financially accessible solutions. Collaborative robots (cobots), whose installations are growing dynamically, and autonomous mobile robots (AMRs) in intralogistics, offering a return on investment in as little as two years, are gaining popularity.

-

Impact on the Labor Market: Forecasts indicate that by 2025, automation will account for over half of the working hours in industry. However, this process does not mean mass unemployment but rather generates demand for new, specialized skills related to programming, maintenance, and data analysis.

Megatrend II: Artificial Intelligence – The Central Nervous System of Factory 4.0

Artificial intelligence is no longer a technological curiosity but is becoming the foundation of modern production. As many as 93% of industry leaders believe that AI integration provides a significant competitive advantage, and 62% of them have seen a return on investment exceeding 10%.

-

AI in Quality Control: In 2025, key applications of AI include predictive quality control. Advanced algorithms detect anomalies in real-time and forecast potential problems before they occur, automatically adjusting machine parameters. Large Language Models (LLMs), such as ChatGPT, are used for automatic analysis of technical documentation and report generation.

-

Implementation Challenges: The biggest barriers remain technological debt (integrating AI with older MES/SCADA systems) and data silos, which prevent the creation of holistic analytical models.

Megatrend III: Green Transformation – From Regulation to Market Demand

The European Green Deal and decarbonization pressure are becoming a hard business requirement. Access to key European markets will increasingly depend on a company's ability to demonstrate a low carbon footprint.

-

Legal Frameworks and Goals: Poland, as part of its EU commitments, aims to reduce CO2 emissions by 55% by 2030 (compared to 1990). In July 2025, the European Commission announced the next stage of the strategy, prioritizing green investments in industry.

-

Circular Economy (CE): The European Union is accelerating the transition to a circular economy, which opens up new financing opportunities for Polish companies. An example is the

"European Funds for Subcarpathia" program, offering grants to SMEs for implementing CE solutions, with applications open until September 30, 2025.

Sectoral Analysis: Innovations in Key Polish Industrial Hubs

-

Heavy and Aerospace Industry (Subcarpathian Region): Subcarpathia is strengthening its position as a center of excellence in advanced manufacturing. In September 2025, the MTU Aero Engines Polska plant in Tajęcina assembled its 5,000th low-pressure turbine module for engines powering Airbus A320neo aircraft. As the world's sole supplier of this component, the Polish plant is a key link in the global aerospace supply chain.

-

Electronics Manufacturing: From August 1, 2025, the new EU standard EN 18031 comes into force, imposing strict cybersecurity requirements. At the same time, through-hole technology (THT) remains indispensable in industrial and military production, guaranteeing higher mechanical strength and temperature tolerance than the SMT technology dominant in consumer electronics.

-

Metal Processing (Silesian Region): Silesia, the heart of Polish industry, is becoming an arena for the convergence of traditional and modern techniques. 3D printing with metal is no longer just a prototyping tool but a viable method for producing final parts with complex geometries. Simultaneously, technologies like

roboforming (robotic sheet metal forming) are introducing a new level of precision in traditional processes.

-

Wood and Furniture Industry (Greater Poland Region): Poland remains a European leader in furniture production, accounting for 30% of upholstered furniture production in the EU. However, the industry, heavily concentrated in Greater Poland, is facing a loss of competitiveness based on old advantages. The way forward is through innovation –

AI used for intelligent wood sorting and robotic lines for processing and milling.

-

Printing and Packaging (Mazovian and Łódź Regions): The industry is undergoing a profound transformation. Digital printing now accounts for 50% of the market. As many as 62% of companies have implemented workflow automation, using web-to-print systems and cost estimation software. A key trend, driven by consumer demand, is

sustainability – the use of recycled paper and biodegradable materials.

Strategic Conclusions for Polish Industry

The Polish industry is on the cusp of a new era. To compete effectively on the global market, companies must adopt a model based on three pillars: advanced technology, high efficiency, and low emissions.

-

Investment in Automation: It is urgent to close the "automation gap" with regional competitors by implementing accessible technologies like cobots and AMRs.

-

AI as an Optimization Tool: It is necessary to move beyond pilot projects and implement AI to optimize resource consumption, predictive quality control, and achieve sustainability goals.

-

Sustainability as a Commercial Necessity: Treating ESG and CE requirements not as a burden but as a condition for access to demanding European markets is crucial for maintaining and growing exports.

Adaptation to these trends will determine which Polish enterprises will shape the future of the industry and which will be left behind.

Content added:

BIAŁCZYK Sp. z o.o.

BIAŁCZYK Sp. z o.o.

News

Fuel crisis 2026: What it means for Europe’s metalworking industry

Fuel Crisis 2026 is increasing costs across Europe’s metalworking industry. Learn the main risks and used machinery opportunities. Read more

Industrial Refrigeration in Poland’s Food Industry: Why Modernization Matters Now

Poland’s food industry is increasing investment in machinery modernization and automation, while the EU’s new F-gas rules are pushing food manufacturers to review refrigeration equipment more carefully. As a result, industrial refrigeration is becoming a strategic upgrade area for companies that want better efficiency, compliance, and long-term production reliability Read more

Buyer's Guide: How to Choose the Right CNC Lathe for Your Shop

Choosing a CNC lathe is one of the most important investment decisions in any metalworking shop. Whether you're starting a business or expanding your machine fleet, the purchase requires analyzing many technical and economic parameters. Read more

How European Metalworking Shops Can Win in the New Industrial Era

European metalworking companies can leverage reindustrialisation, nearshoring and booming demand in energy, e‑mobility and defence to move into higher‑margin, long‑term contracts. By specialising, upgrading their machine park (including with used machines) and professionalising quality and sales, they can modernise quickly with support from platforms like wesellmachines.com led by eng. Marcin Białczyk Read more

What is currently happening in the European industry at the turn of February 2026?

Discover how the rising PMI index and the new EU Industrial Accelerator Act impact machine valuation in 2026. Appraiser Marcin Białczyk from wesellmachines.com analyzes market trends, replacement value, and functional obsolescence of CNC equipment in the Industry 4.0 era. Read more

The Green Steel Revolution: A Strategic Analysis of Industrial Transformation

Strategic analysis of the steel sector's shift to green steel. Expert Marcin Białczyk explores DRI and EAF technologies, Fit for 55, CBAM, and industrial machinery valuation challenges in the era of decarbonization and ESG requirements. Read more

Valuation of Modern Tube and Profile Bending Machines in 2026

Marcin Białczyk (wesellmachines.com) redefines CNC bender valuation for 2026. Key takeaway: All-Electric technology and IIoT data drive higher residual value through extreme precision (±0.05°) and energy efficiency (50% savings). The guide bridges technical appraisal with 2026 funding paths (FENG, BGK) for the manufacturing sector. Read more

Nail Machine Valuation: What Are You Actually Buying? Expert Analysis

In my daily work at WeSellMachines, I frequently encounter a question that, on the surface, seems entirely rational: "Marcin, why does this 20-year-old Wafios automatic machine cost €40,000, when I can get a brand new machine with similar output from an Asian importer for €15,000?" Read more

How to Buy a Used Multi-Rip Saw and Revolutionize Your Sawmill

The secondary market for woodworking machinery is vast but full of traps. As an expert who has seen hundreds of machines "painted for sale" but destroyed on the inside, I have prepared this comprehensive guide for you. This isn't marketing fluff, but a solid dose of engineering knowledge that will allow you to independently assess the technical condition of a machine. Read more

The End of the "Cheap Furniture" Era? Your Survival and Growth Strategy for 2026–2030

For decades, the Polish wood and furniture industry has been the undisputed leader in exports, generating an impressive €16.3 billion in 2024. We were the "furniture factory for Europe," winning on price, raw material availability, and skilled labor. However, as a practitioner who visits your plants daily, I see it clearly: this model is running out of steam. Read more

Executive Summary: The State of Play for 2025

The metalworking sector is entering a phase defined in macroeconomic analyses as the "Hyper-Efficiency Era." With industrial sentiment indices fluctuating and steel consumption forecasts showing only marginal growth (+2.2%), the margin for investment error has effectively vanished. At wesellmachines.com, we identify a fundamental paradigm shift: a transition from a Growth-at-all-costs strategy to Asset Utilization & Cash Flow Protection. In this report, we analyze why the key to survival in 2025-2026 is not buying "new," but buying "efficient"—often from the secondary market. Read more

How to Choose a Used Wood CNC Machining Center? A Complete Machine Audit Step-by-Step

Buying a used wood CNC machining center is a huge opportunity, but also a massive risk. Pervasive MDF dust destroys key components, and the cost of repairing a spindle or vacuum pump is staggering. This complete guide (5000+ words) is a professional technical audit in a nutshell. We will teach you how to inspect the machine step-by-step—from spindle diagnostics and vacuum table leak tests to assessing mechanics and controls. Avoid a costly mistake and make an informed investment with our expert checklist. Read more

The Complete Guide: How to Buy a Used CNC Press Brake and Not Regret the Investment

Buying a used CNC press brake is a strategic but risky investment. This article is a complete guide that explains, step-by-step, how to conduct a professional technical inspection to minimize risk. The author, an expert with 20 years of experience, describes the key elements to check: from evaluating the frame and hydraulics, through diagnostics of the CNC control, to verifying the completeness of the documentation. The article provides the necessary knowledge to make an informed and safe decision, helping to avoid costly mistakes. Read more

")

AI in European Industry: How Artificial Intelligence Shapes New Roles for Managers and Specialists (Competencies 2026)

The impact of Artificial Intelligence (AI) is a pivotal topic across the entire European manufacturing sector. From German automotive to French chemicals, enterprises throughout the European Union are actively implementing AI and Machine Learning (ML) solutions, leading to a revolution in job roles. This article analyzes how AI is transforming the roles of managers and specialists, shifting from routine tasks to predictive analytics and strategic system management. We outline the essential competencies needed to thrive in the era of Industry 5.0. Read more

and Avoiding Legal Penalties")

Technological Audit of the Machine Park: Key to Increasing Efficiency (OEE) and Avoiding Legal Penalties

The technological audit is a strategic tool that allows companies to transform their equipment into a business asset. It focuses on 3 pillars: technology, processes (CT loss reduction, OEE), and Compliance (adherence to EU law). Regular investment leads to TCO reduction and increased machine lifespan, ensuring decisions are based on facts, not guesswork. Read more

Log in with Facebook

Log in with Facebook Log in with Google

Log in with Google